Industrial underwriting

Physical Underwriting for Industrial Buildings: Roof, Paving, Drainage, and Envelope Risk

Industrial building risk does not stop at the roof edge. This guide shows buyers, lenders, brokers, insurers, roofers, owners, and asset managers how to connect roof, paving, drainage, dock, and envelope evidence before capex surprises appear.

Key takeaways

- Industrial physical underwriting should connect roof, paving, drainage, dock, envelope, records, tenant use, weather exposure, and consequence.

- Truck court paving, dock aprons, stormwater paths, wall joints, and roof drainage can change capex confidence as much as roof age.

- A useful file separates known maintenance, known repair, uncertain condition, and capital correction instead of blending exterior systems into one vague reserve.

- Weather records should adjust inspection priority and record requests, but they do not prove property-specific roof, paving, drainage, or envelope damage by themselves.

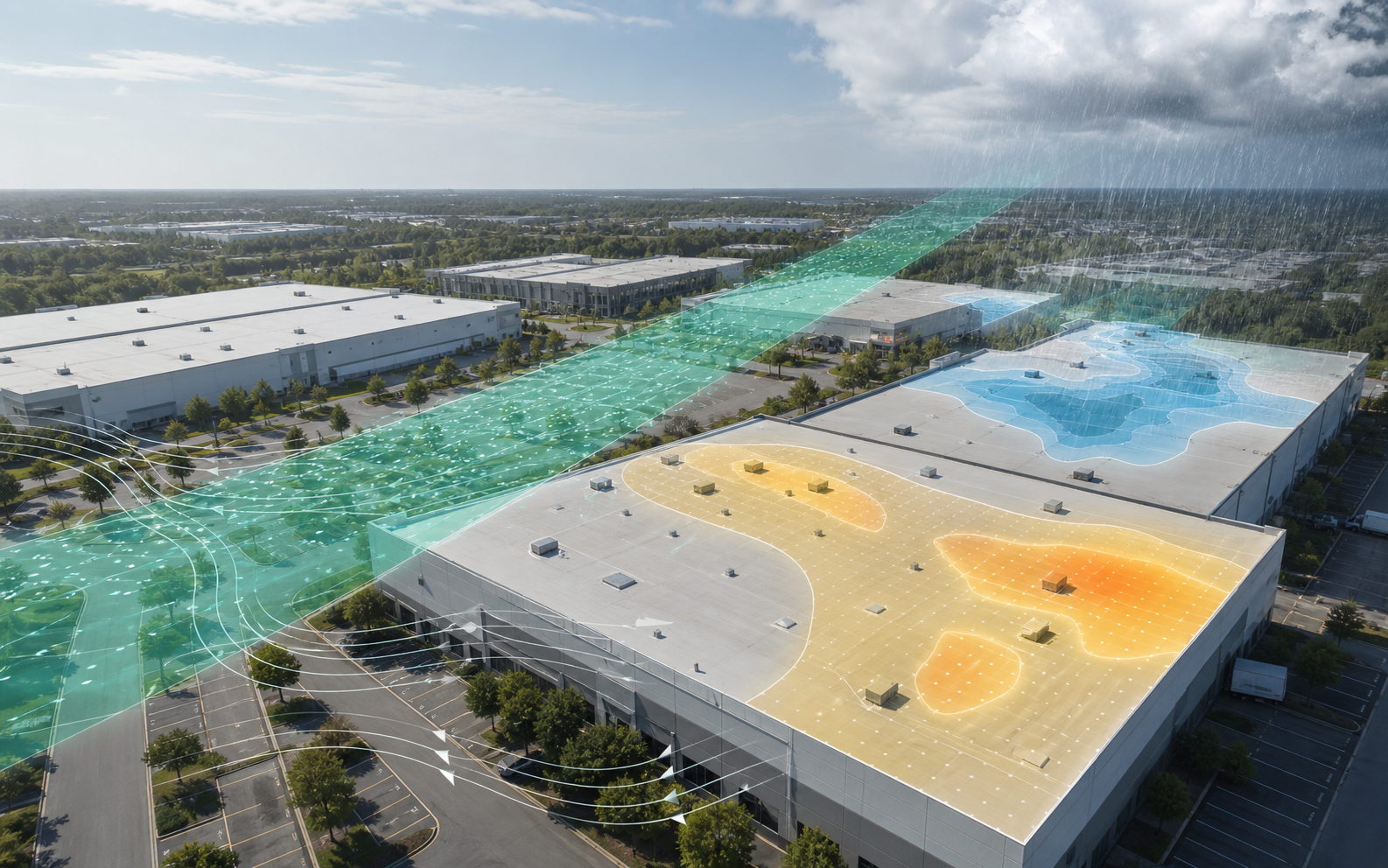

Industrial physical underwriting is not a single building score

Industrial buildings often look simple from the outside: a large roof, concrete or metal wall panels, dock doors, a truck court, parking, stormwater paths, and tenant equipment. That simplicity can make physical underwriting too thin. A warehouse may be described by square footage, clear height, dock count, age, tenant use, roof age, and location. Those fields matter, but they do not explain how the asset will behave when water, traffic, weather, and deferred maintenance start interacting.

The useful question is not only whether the building is in good condition. The useful question is whether roof, paving, drainage, and envelope evidence is strong enough for the decision being made. A buyer, lender, broker, insurer, developer, owner, or asset manager may need a different answer depending on the transaction, tenant, loan, lease, renewal, reserve, or capital plan. An industrial building can be desirable and still carry physical uncertainty that changes price, timing, lender conditions, insurance follow-up, or owner capex.

Asset Optimix treats industrial physical underwriting as a connected exterior-risk file. The roof controls water above the tenant. Paving controls truck operations, drainage, access, and curb appeal. Site drainage connects roof water, stormwater paths, dock areas, pavement life, and tenant interruption. The envelope controls water entry, air leakage, panel movement, facade deterioration, and the condition of openings. These systems do not fail in isolation.

A roof leak can appear first as a tenant complaint. A blocked roof drain can send water toward a wall or overflow path. Poor truck-court drainage can accelerate pavement distress and create dock-access issues. Wall-panel joints can create moisture paths that look like roof leaks. Repeated trailer impact can damage dock doors and aprons. A clean roof age field does not answer those questions. A broad property condition assessment may not map them in enough detail for a high-consequence decision.

Industrial physical underwriting should separate hazard, vulnerability, observed condition, operations consequence, record quality, and next action. That structure keeps a visible crack from becoming panic, and it keeps a clean aerial photo from becoming false comfort.

The four exterior systems should be reviewed together

The exterior physical file for an industrial building should treat roof, paving, drainage, and envelope as one operating system. Each component has its own inspection logic, but the financial risk often comes from their interaction.

Roof evidence includes age by section, system type, drainage, rooftop equipment, penetrations, edge conditions, prior repairs, weather exposure, tenant leak history, warranty documents, and current photos. A roof can be a planned reserve item or an immediate diligence issue depending on record quality and consequence.

Paving evidence includes truck-court asphalt or concrete condition, dock aprons, trailer parking, turning radii, fire lanes, curb and gutter, potholes, cracking, rutting, settlement, striping, pavement drainage, and repair history. Paving is not just a cosmetic site item for industrial properties. It can affect truck movement, tenant operations, leasing, safety management, and replacement timing.

Drainage evidence includes roof drains, scuppers, gutters, downspouts, storm inlets, catch basins, surface flow, detention or retention areas, swales, loading-dock ponding, perimeter grading, and evidence of sediment, staining, erosion, or standing water. Drainage is the bridge between roof and paving.

Envelope evidence includes wall panels, masonry, precast joints, metal panel seams, dock doors, personnel doors, windows, louvers, penetrations, sealant joints, parapets, roof-to-wall transitions, impact damage, facade staining, and interior water evidence. The envelope decides whether wind-driven rain, maintenance gaps, panel movement, and tenant operations become interior consequences.

When these systems are reviewed separately, the file can miss the real issue. A dock-area water complaint may be treated as pavement when roof downspouts discharge nearby. A ceiling stain may be treated as roof when wall-panel joints are open. A pavement reserve may ignore storm inlets that are clogged or low. A roof replacement plan may miss parapet, wall, and drainage details that change scope.

The industrial underwriting file should force the question: where do these systems meet?

Industrial roof risk depends on use, access, and consequence

Industrial roof risk is not only a roof-age question. A low-slope warehouse roof with a documented installation date can still carry high uncertainty if rooftop equipment is dense, drains are poorly documented, tenant leak history is unclear, or weather exposure occurred after the last inspection. Another roof may be older but easier to underwrite because maintenance records, section maps, and current photos are strong.

Industrial roofs often include large areas with internal drains, parapets, mechanical units, exhaust fans, skylights, smoke vents, solar attachments, pipe supports, tenant penetrations, and access paths. Those details change risk. A distribution tenant with heavy rooftop HVAC service traffic may create different conditions than a simple storage user. A food, cold-storage, manufacturing, or laboratory tenant may add rooftop equipment and interior consequence. A vacant building may have fewer work orders but more uncertainty because nobody is reporting small leaks.

The roof file should answer:

- What roof sections exist?

- What age evidence supports each section?

- What system type and work scope are documented?

- Where are drains, scuppers, gutters, and overflow paths?

- Which equipment areas create traffic or drainage interruption?

- What leak tickets or tenant complaints exist?

- What repairs were made, where, and when?

- What photos are current?

- What roof areas were not accessed?

- What weather exposure occurred after the last condition file?

The [roof age confidence bands guide](/insights/commercial-roof-age-confidence-bands/) explains why industrial roof age should be treated as an evidence field, not a single certainty. The [commercial roof inspection photo checklist](/insights/commercial-roof-inspection-photo-checklist/) gives a practical way to make the current roof file usable.

For industrial underwriting, the roof decision should land in one of several actions: monitor, maintain, inspect, repair, test for moisture, refresh bids, adjust reserve, require seller response, or plan capital intervention. The action should match evidence, not anxiety.

Paving risk is operational risk

Paving is often underweighted in industrial acquisitions because it looks like site work rather than building work. That is a mistake. Truck courts, dock aprons, trailer parking, employee parking, fire lanes, access drives, and concrete pads can affect tenant operations and replacement timing. Paving distress can also reveal drainage problems that will not be obvious from a roof review.

Industrial paving distress may include potholes, alligator cracking, longitudinal cracking, transverse cracking, rutting, shoving, settlement, edge breakdown, joint failure, ponding, spalling concrete, broken dock aprons, depressed utility patches, failed trench repairs, poor striping, and damaged curbs. The concern is not that every crack is urgent. The concern is whether distress aligns with truck traffic, drainage, tenant consequence, and reserve assumptions.

Truck courts deserve a separate pass. A lightly used employee lot and a high-traffic truck apron should not be reviewed as the same paving asset. Trailer turning, loading patterns, snow removal, heavy axle loads, dropped trailers, and dock activity can accelerate distress. A building marketed as logistics-ready can lose value if truck court paving is failing or if drainage makes dock operations unreliable.

The paving file should answer:

- Which paved areas are asphalt, concrete, gravel, or mixed?

- Which areas carry heavy truck traffic?

- Where are dock aprons and trailer parking?

- Where are cracks, potholes, rutting, settlement, or patches concentrated?

- Does distress align with ponding or drainage paths?

- Are storm inlets, curbs, and gutters functioning?

- What repairs have already been made?

- Is the reserve based on pavement area, traffic intensity, and condition?

FHWA pavement preservation guidance is useful background because it reinforces the practical idea that timing and condition matter. A pavement surface that receives maintenance before major structural failure is different from pavement where deferred work has moved into reconstruction territory. For industrial underwriting, the question is how far along that path the property appears to be.

Site drainage connects roof, paving, docks, and envelope

Drainage is the connective tissue of industrial physical risk. Roof water leaves the roof. Paved surfaces move stormwater. Loading docks often sit below surrounding grades. Wall panels, dock doors, and personnel doors are vulnerable where water stands or flows. Storm inlets, swales, detention areas, and outfalls influence whether water is controlled or trapped.

The file should show how water moves through the site. That does not require a full engineering model for every diligence event, but it does require more than a dry-day aerial. Look for visible flow paths, roof discharge, scuppers, downspouts, sheet flow across pavement, ponding at docks, sediment at inlets, erosion at swales, staining on walls, and water marks near doors.

Loading docks are high-consequence drainage locations. Ponding at dock doors can interfere with operations, damage door components, create interior water entry, and accelerate pavement distress. A dock area can appear functional in a listing photo and still have water-management problems after heavy rain. Buyers and lenders should ask whether dock-area drainage was observed, whether photos were taken after rain, and whether tenant work orders mention water at loading areas.

Roof drainage also matters. Internal roof drains can discharge into storm systems that affect site drainage. Scuppers and downspouts may discharge near paved areas, landscaped strips, or wall bases. If roof drainage is clogged or redirected, the site may show symptoms: staining, erosion, ponding, facade streaking, or repeated pavement repairs.

The [roof drains, scuppers, ponding water, and hidden capex guide](/insights/commercial-roof-drainage-ponding-hidden-capex/) covers the roof side of this issue. Industrial underwriting should extend the same discipline to the ground plane.

Envelope risk is not just facade appearance

Industrial building envelopes can look repetitive and robust, but the details matter. Wall panels, precast joints, masonry, metal panels, tilt-up panels, dock doors, personnel doors, windows, louvers, roof-to-wall transitions, parapets, and sealant joints can all create water or air paths. Envelope issues may show up as interior staining, tenant complaints, corrosion, damaged finishes, pest pathways, energy issues, or recurring maintenance.

Envelope review should include:

- Wall-panel joints and sealant condition.

- Parapet and coping transitions.

- Roof-to-wall flashing.

- Dock doors and dock seals.

- Personnel doors and thresholds.

- Windows, louvers, vents, and wall penetrations.

- Impact damage from trailers, forklifts, or vehicles.

- Facade staining, cracks, spalling, corrosion, or displaced panels.

- Interior wall staining or insulation exposure.

The mistake is treating the envelope as a visual item only. A clean facade in a marketing photo may not show open sealant joints at parapets, damaged dock seals, or water entry at door thresholds. A small wall joint issue can matter if it sits above sensitive tenant operations or if it repeats across a long elevation.

The envelope also influences roof decisions. A roof replacement or restoration can fail to solve leaks if roof-to-wall transitions or wall-panel joints remain open. A roof leak ticket may actually trace to wind-driven rain at a wall. A reserve plan that includes roof and paving but ignores envelope joints can still miss recurring water-entry cost.

WBDG building-envelope and moisture-management guidance supports the practical premise that exterior moisture control is an assembly issue, not a single product issue. Industrial underwriting should reflect that by tying envelope evidence to roof, drainage, and interior history.

Dock areas are their own underwriting zone

Dock areas concentrate risk because roof, paving, envelope, drainage, doors, operations, and tenant activity converge there. A dock wall has openings. The pavement takes turning, braking, trailer loads, snow work, and water flow. Dock aprons can crack, settle, spall, or hold water. Door seals can fail. Bollards and guards can be damaged. Interior spaces behind dock doors may show water entry, impact, or operational wear.

The dock file should show:

- Wide view of the dock elevation.

- Dock apron condition.

- Door and seal condition.

- Pavement slope and ponding.

- Storm inlets near dock areas.

- Wall staining or impact damage.

- Interior door threshold evidence.

- Trailer parking and turning patterns.

- Bollard, curb, and guard conditions.

- Repairs or tenant complaints tied to docks.

Dock distress can change leasing and capex discussions. A buyer underwriting a warehouse for logistics use may treat dock reliability as central to the asset. A lender may not want dock-area paving distress hidden inside a generic site-improvement reserve. An insurer or risk engineer may care about water entry, traffic, and physical damage patterns.

Do not overstate dock photos. A cracked apron photo does not prove structural failure. A water stain does not prove a specific source. A damaged dock seal does not prove tenant interruption. The file should identify visible evidence and the next needed review.

Tenant use changes the exterior risk profile

Industrial buildings are not interchangeable. Tenant use changes the way physical systems age. Distribution, cold storage, food processing, light manufacturing, heavy manufacturing, contractor yards, last-mile delivery, wholesale, automotive, and public works uses can create different roof, paving, drainage, and envelope conditions.

Tenant use affects:

- Rooftop equipment quantity and service frequency.

- Interior humidity and exhaust requirements.

- Drainage sensitivity and dock activity.

- Truck court loads and turning patterns.

- Trailer parking and yard use.

- Door impact and dock-seal wear.

- Utility penetrations and wall openings.

- Maintenance access.

- Consequence of water entry.

A roof over refrigerated storage may have different consequence than a roof over dry bulk storage. Paving under constant trailer use may age differently than a lightly used lot. Envelope penetrations for industrial exhaust may change water-entry risk. Drainage at a food or cold-storage dock may matter more if water entry affects operations or sanitation concerns.

The underwriting file should ask what the building is used for now, what it was used for before, and what the buyer expects to use it for next. A building may be acceptable for one tenant profile and capital intensive for another. That does not make the asset bad. It means use-specific physical evidence matters.

Weather exposure should adjust inspection priority, not replace evidence

Weather records help explain exposure, but they do not prove property-specific condition. Severe wind, hail, heavy rain, snow load concerns, freeze-thaw cycles, heat, and tropical rainfall can all stress industrial roof, paving, drainage, and envelope systems. The correct use of weather history is to adjust inspection priority, record requests, and reserve confidence.

For example, severe wind exposure may raise priority for edge metal, rooftop equipment, parapets, doors, and wall panels. Heavy rainfall may raise priority for roof drains, scuppers, storm inlets, dock-area ponding, and interior stains. Freeze-thaw exposure may influence pavement cracking, spalling, sealant, and drainage maintenance. Heat may influence roof membrane aging and asphalt distress. Hail exposure may raise roof and rooftop equipment questions, but it still requires property-specific evidence.

The [roof weather risk and physical underwriting guide](/insights/roof-weather-risk-physical-underwriting/) explains this evidence boundary in detail. Industrial underwriting should apply the same rule across exterior systems: weather is exposure context, not a conclusion by itself.

The file should connect exposure to response:

- Was the building inspected after the event?

- Were roof drains and site inlets checked?

- Were dock areas or tenant spaces affected?

- Were repairs made?

- Were photos taken before and after cleanup?

- Did tenant complaints increase?

- Did insurance, lender, or owner records mention the event?

If the answer is unknown, confidence should drop until current evidence is available.

Records can change the risk more than age

Industrial physical underwriting depends on record quality. A building with older components and strong records can be easier to underwrite than a newer building with vague statements. Records turn unknown condition into labeled uncertainty.

Useful records include:

- Roof age evidence by section.

- Roof replacement, recover, coating, restoration, and repair scopes.

- Roof warranties and maintenance duties.

- Roof inspection photos and leak logs.

- Drain maintenance and storm-response notes.

- Pavement bids, repairs, and resurfacing history.

- Dock apron repairs and tenant complaints.

- Stormwater maintenance records where available.

- Envelope sealant, facade, door, and panel repairs.

- Property condition assessments and reserve schedules.

- Tenant work orders related to water, doors, docks, roof, or paving.

- Capital budgets and deferred-maintenance lists.

ASTM property-condition assessment framing and Fannie Mae PCA guidance are useful because they emphasize observed condition, useful life, repairs, and reserves. But a broad PCA can still leave industrial-specific questions open. If roof access was limited, pavement was snow-covered, dock drainage was not observed after rain, or envelope joints were not reviewed closely, the file should say so.

The underwriting question is not whether a record exists. It is whether the record supports the decision. A roof invoice without section mapping may be weak. A paving bid without square footage or scope may be incomplete. A PCA with a remaining useful life estimate but no current drain photos may not be enough for a high-stakes acquisition.

Mixed vintages and additions can hide the weakest area

Industrial buildings often grow over time. A warehouse may start as one box, then add office space, a cooler, a mezzanine, a manufacturing bay, a canopy, a truck-court expansion, a trailer yard, or a new dock wall. The records may still describe the property as though it is one building. That can make physical underwriting misleading.

Mixed vintages show up in several ways:

- Different roof sections with different installation dates.

- Additions with different wall panels or structural systems.

- Older dock aprons beside newer paving.

- Utility trenches and patched pavement from tenant improvements.

- Different drainage patterns by expansion area.

- Parapet or wall transitions between old and new sections.

- Abandoned roof curbs or penetrations from prior tenant use.

- Pavement areas designed for lighter use than current truck traffic.

The file should not average these conditions into one building age. A newer addition can create a roof-to-wall transition that leaks. An older truck court can drive near-term capex even when the roof is newer. A recently paved employee lot can make the site look better while the dock apron remains distressed. A newer wall section can hide an older roof section behind it.

For buyers and lenders, the practical move is to map the building by physical zones. Label main warehouse, office, additions, dock wall, truck court, trailer area, employee parking, yard, and detached structures. Then attach roof, paving, drainage, and envelope evidence to each zone. The smallest or oldest zone may be the one that changes the reserve. The most visible zone may not be the most important one.

For brokers, mixed vintages are a language risk. "2019 roof" may apply only to one section. "Recently paved" may mean an employee lot, not the truck court. "Expanded in 2021" may mean new operational value but new roof and envelope transitions. Better diligence language separates zones and scope.

Stormwater evidence needs ground-level photos

Industrial drainage cannot be understood from roof photos alone. The roof may drain correctly while the truck court ponds. The truck court may look acceptable when dry while dock doors receive water during heavy rain. A storm inlet may appear present on an aerial but be clogged, sunken, damaged, or poorly located relative to flow.

Ground-level stormwater photos should show:

- Catch basins and inlet grates.

- Curb lines and gutter flow.

- Low points in truck courts and trailer areas.

- Loading-dock slopes and trench drains where present.

- Ponding marks, sediment, staining, algae, or debris.

- Downspout discharge locations.

- Swales, detention areas, and outfall paths where visible.

- Erosion or soil movement near paved edges.

- Water marks at dock doors, wall bases, and thresholds.

The file should distinguish dry-day evidence from wet-weather evidence. A dry photo of a storm inlet can show condition and access. A wet photo can show whether water reaches it, bypasses it, or overwhelms it. A post-cleaning photo can show whether maintenance corrected the concern. Without sequence, stormwater evidence can be easy to misread.

Stormwater evidence also matters for pavement life. Water standing at cracks, joints, and pavement edges can accelerate distress. Poor drainage at dock areas can create both operations risk and capital risk. If a truck court has repeated patching in the same low area, the paving issue may not be solved by another patch. The drainage path may need review.

The underwriting file should not make engineering conclusions from photos. It should identify where water evidence is strong enough to justify maintenance, qualified review, bid refresh, or reserve adjustment.

Roof and paving reserves should not be blended into one vague line

Industrial reserves often become too broad. A file may include one line for "site improvements" or one near-term number for "roof and paving." That can be acceptable for a rough early screen, but it is weak when the decision depends on capital timing. Roof, paving, drainage, dock, and envelope costs behave differently.

Roof work may depend on membrane system, insulation, deck condition, drainage correction, rooftop equipment, access, phasing, and tenant sensitivity. Paving work may depend on asphalt versus concrete, truck loads, base condition, drainage, milling depth, concrete apron work, striping, curbs, and operational sequencing. Drainage work may involve inlet cleaning, pipe issues, grading, trench drains, outfalls, or design review. Envelope work may involve sealant programs, panel repairs, doors, dock seals, parapets, or wall penetrations.

Blending these costs can hide the actual decision. A property with a near-term truck-court resurfacing need and a medium-term roof reserve is different from a property with a near-term roof replacement need and routine paving maintenance. A lender, buyer, or asset manager should be able to see the intervention path.

A better reserve table separates:

| Reserve line | Evidence basis | Timing question |

|---|---|---|

| Roof | Age, current photos, drains, leaks, repairs, moisture concern | Repair, restore, test, or replace |

| Paving | Distress map, truck areas, drainage, bids, repairs | Seal, patch, mill, overlay, reconstruct |

| Drainage | Roof discharge, inlets, ponding, grading, dock water | Maintain, clean, review, redesign |

| Dock and doors | Aprons, seals, doors, impact damage, tenant complaints | Repair, replace, coordinate with tenant |

| Envelope | Joints, panels, penetrations, staining, interior evidence | Local repair or broader program |

This separation does not require perfect pricing on day one. It requires transparent uncertainty. If the paving scope is unknown, say so. If roof moisture is untested, say so. If dock drainage could change both paving and door repairs, say so. Vague reserve lines are where late surprises hide.

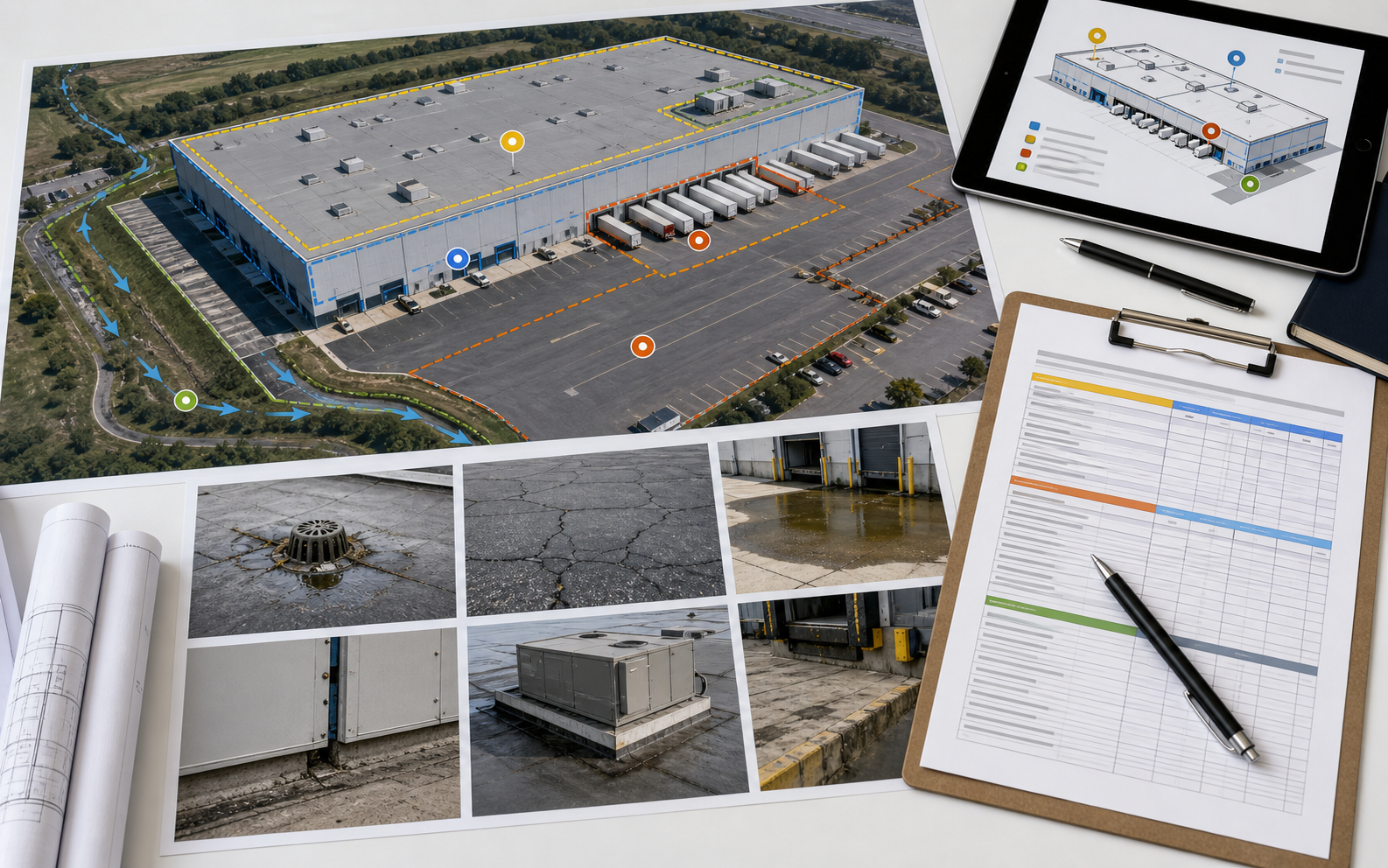

A 30-day industrial diligence sequence

Industrial physical diligence often moves quickly. A practical 30-day sequence can prevent the exterior file from becoming a last-minute scramble.

In the first week, gather existing records. Ask for roof age evidence by section, recent roof photos, leak logs, roof repair invoices, paving bids, site maintenance records, dock repair history, envelope repairs, tenant work orders, prior PCA material, and known capital plans. Create a zone map for roof, paving, drainage, docks, and envelope.

In the second week, review current photos and identify gaps. Are all roof sections visible? Are truck courts and dock aprons separated from employee parking? Are storm inlets and ponding areas photographed? Are wall joints, doors, and parapets visible? Are interior stains mapped? Are records tied to locations? If not, request targeted photos or schedule qualified review.

In the third week, separate known items from uncertainty. Known items may include a recent roof repair, a paving bid, a dock door replacement, or a sealant program. Uncertainty may include unknown roof age, stale photos, unexplained water entry, pavement distress without scope, or stormwater concerns without wet-weather evidence. Assign each item a likely next action.

In the fourth week, connect the exterior file to the business decision. Does the buyer need a seller credit, reserve adjustment, inspection contingency, bid refresh, lender discussion, or closing condition? Does the lender need a repair escrow or monitoring item? Does the broker need cleaner seller language? Does the owner need a maintenance action before the next tenant or renewal event?

This sequence is simple, but it prevents a common failure: waiting for a broad PCA summary and then discovering that roof, paving, drainage, and envelope questions were not answered at the level the transaction requires.

A practical evidence matrix

Industrial physical underwriting improves when evidence is organized by system, consequence, and action. A matrix keeps the file from becoming a loose collection of concerns.

| System | Evidence to gather | What it changes |

|---|---|---|

| Roof | Age by section, drains, equipment, repairs, leak history, photos | Inspection priority, reserve timing, repair scope |

| Paving | Truck court condition, dock aprons, cracks, rutting, ponding, repairs | Tenant operations, capex, access, leasing risk |

| Drainage | Roof discharge, storm inlets, ponding, grading, dock water, erosion | Hidden cause, maintenance, engineering review priority |

| Envelope | Wall joints, doors, panels, parapets, penetrations, interior stains | Water-entry risk, repair planning, roof-leak attribution |

| Records | PCA, invoices, warranties, work orders, photos, bids | Confidence, negotiation, lender conditions |

| Weather | Rain, wind, hail, freeze-thaw, heat exposure, response actions | Freshness of evidence, inspection timing |

This matrix should not produce a generic score. It should produce a next action. A property may need updated photos, a roofer visit, pavement scope, drainage review, envelope repair bid, seller document request, reserve adjustment, or lender discussion. The right next action depends on evidence and consequence.

Buyer diligence should price known cost and uncertainty separately

Industrial buyers should separate known capital cost from uncertainty. A known roof repair, known pavement bid, or known dock-door repair can be priced directly. Unknown drainage cause, undocumented roof age, stale pavement photos, or unexplained interior staining should be priced as uncertainty until evidence improves.

Four buckets help:

| Bucket | Industrial example | Decision use |

|---|---|---|

| Routine maintenance | Clear drains, clean inlets, seal minor pavement cracks | Operating plan |

| Known repair | Repair scupper flashing, replace dock seal, patch pothole | Seller credit or near-term scope |

| Uncertain condition | Ponding at docks with no rain follow-up, unknown roof section age | Inspection, testing, reserve contingency |

| Capital correction | Roof replacement, truck-court resurfacing, drainage redesign, envelope joint program | Capex plan and lender discussion |

This structure prevents two mistakes. The first is ignoring uncertainty because no bid exists. The second is treating every visible issue as a full replacement problem. A buyer should ask what evidence would move an item from uncertain to known.

For time-constrained acquisitions, especially exchange-driven purchases, this matters. The [commercial roof records before a 1031 exchange acquisition guide](/insights/commercial-roof-records-1031-exchange-acquisition/) explains why roof records should be gathered early. Industrial buildings add paving, drainage, and envelope records to that same timing problem.

Lenders need scope confidence, not broad reassurance

Industrial lenders may receive a PCA, borrower statements, broker materials, roof age, and reserve recommendations. Those inputs can be useful, but the lender still needs to know whether major exterior systems are understood at a level appropriate to the loan.

A lender should look for:

- Whether all roof areas were accessed or documented.

- Whether roof drainage and leak history were reviewed.

- Whether paving condition reflects truck use and dock operations.

- Whether site drainage and dock ponding were considered.

- Whether envelope water-entry evidence was reviewed.

- Whether reserves separate roof, paving, drainage, envelope, and dock items.

- Whether immediate repairs are actually immediate or simply visible.

- Whether cost estimates are current enough for the market.

The concern is not only collateral condition. It is borrower surprise. A loan that underestimates exterior capex can create pressure after closing. A reserve that lumps paving and roof into a broad line may not match the actual intervention path. A building with strong tenant operations can still carry exterior system risk that deserves conditions or monitoring.

Lenders do not need to become roofers, paving consultants, or envelope specialists. They need the file to show where the conclusion comes from and where uncertainty remains.

Brokers can make industrial diligence faster without overclaiming

Brokers can reduce deal friction by organizing exterior physical evidence before launch. That does not mean certifying condition. It means preparing a file that avoids vague claims and late surprises.

A broker pre-listing file for an industrial building should include:

- Roof area map and current roof photos.

- Drainage photos for roof and site.

- Paving photos separated by employee parking, truck court, dock apron, and trailer areas.

- Dock door, dock seal, and dock apron photos.

- Envelope photos at walls, joints, doors, parapets, and penetrations.

- Known leak logs and tenant work orders.

- Repair invoices and bids.

- PCA excerpts if available.

- Warranty or maintenance obligations.

- Access limits and missing records.

The [broker listing diligence guide](/insights/commercial-roof-broker-listing-diligence/) covers roof-specific pre-listing discipline. For industrial properties, the same idea extends to the yard and envelope. A buyer will likely ask about truck court, dock condition, roof age, drainage, and water history. A broker who has the file ready can move faster and avoid overstating what the seller knows.

Language matters. "Well-maintained industrial building" is broad. "Seller provided 2025 roof maintenance photos, 2024 truck-court repair invoice, current dock-area photos, and no reported active roof leaks; west dock drainage follow-up pending" is more useful and more defensible.

Insurers and risk engineers should look for interaction patterns

Insurance teams, risk engineers, and loss-control reviewers often think across systems: water intrusion, wind vulnerability, maintenance control, fire access, tenant operations, and business interruption. Industrial exterior files should help them see interaction patterns.

Useful patterns include:

- Roof drains plus interior leak tickets below the same area.

- Wind exposure plus edge, parapet, door, or rooftop equipment concerns.

- Heavy rainfall plus dock ponding and storm-inlet maintenance gaps.

- Truck court pavement distress plus poor surface drainage.

- Envelope staining plus roof-to-wall transition gaps.

- Tenant process humidity plus roof or wall condensation concerns.

- Repeated equipment service plus roof membrane traffic damage.

The key is evidence separation. A pattern is not proof by itself. It is a reason to prioritize review, maintenance, or documentation. An insurer should not treat weather exposure as damage proof, and an owner should not treat absence of a claim as proof of no physical issue. A risk review is strongest when it labels observed condition, exposure, vulnerability, consequence, and open unknowns.

Owners and asset managers need reserve triggers

Industrial exterior reserves should not be static guesses. They should include triggers that tell the owner when to refresh scope or funding. Roof, paving, drainage, and envelope systems often move from maintenance to capital planning through visible thresholds.

Examples:

- Roof leaks recur in the same area after repairs.

- Ponding remains after drain or inlet cleaning.

- Truck-court potholes reappear in patched areas.

- Dock apron settlement affects trailer movement.

- Wall-panel joint failures repeat along one elevation.

- Door thresholds or dock areas show recurring water entry.

- Paving bids shift from maintenance to resurfacing or reconstruction.

- Roof moisture testing confirms wet insulation.

- Major weather exposure occurs after the last condition file.

- Tenant use changes and increases rooftop equipment or yard traffic.

Each trigger should have an action. That action may be maintenance, qualified inspection, bid refresh, moisture scan, pavement evaluation, drainage review, envelope repair program, reserve adjustment, or tenant coordination.

The [commercial roof capex and reserve planning guide](/insights/commercial-roof-capex-reserve-planning/) gives the roof-specific reserve framework. Industrial buildings need the same discipline for paving, drainage, and envelope.

What not to conclude from industrial physical evidence

Photos and records can make an industrial building easier to underwrite, but they have limits. A roof photo does not prove hidden moisture is absent. A paving crack does not prove reconstruction is required. A dock puddle does not prove a drainage system is defective. A wall stain does not prove the roof is leaking. A weather event does not prove property-specific damage. A remaining useful life estimate does not prove exact replacement timing.

The file should avoid:

- Engineering conclusions without qualified review.

- Code conclusions from photos alone.

- Warranty conclusions without warranty documents and proper review.

- Insurance coverage conclusions.

- Claims that visible condition proves no hidden defects.

- Claims that age alone proves remaining useful life.

- Claims that one system explains all water entry.

Better language is specific and bounded:

- "Ponding observed at west dock after heavy rain; storm-inlet maintenance history pending."

- "Truck-court cracking concentrated near trailer turning path; pavement scope not yet priced."

- "Roof drains photographed after cleaning; no follow-up after rain in file."

- "Wall-panel staining visible below parapet; source not confirmed."

- "Roof age documented for main field; office addition age unknown."

This kind of language helps everyone. It gives buyers questions, lenders confidence limits, roofers a starting point, brokers safer positioning, and owners a practical next action.

A clean industrial physical file is a business advantage

Industrial buildings compete on location, clear height, access, docks, yard, tenant fit, and reliability. Physical condition does not need to be perfect to support a transaction or loan. It needs to be legible. A roof with known age, current photos, maintenance records, and reserve timing is different from a roof described from memory. A truck court with mapped distress and a current bid is different from a vague paving concern. A dock drainage issue with follow-up photos is different from an unexplained puddle. An envelope repair program is different from repeated untracked water complaints.

The best physical underwriting file connects roof, paving, drainage, and envelope into one decision view. It tells the user what is known, what is observed, what records support it, what consequence exists, and what action should follow. It does not replace qualified inspection or professional judgment. It gives those professionals a better starting point and gives business stakeholders a clearer basis for pricing, lending, insuring, maintaining, or intervening.

For Asset Optimix, that is the reason industrial physical underwriting belongs beside commercial roof intelligence. Roof risk often starts the conversation, but industrial exterior risk rarely stops at the roof edge. The capital plan, tenant plan, and underwriting file need to follow the water, the traffic, the weather, and the records across the whole property.

Frequently asked questions

What is physical underwriting for an industrial building?

It is the process of organizing observed condition, records, exposure, consequence, and capital timing for building systems such as the roof, paving, drainage, dock areas, and envelope. It supports business decisions but does not replace qualified inspection or professional judgment.

Why should paving be part of industrial physical underwriting?

Truck courts, dock aprons, trailer areas, and access drives affect operations, tenant use, drainage, repairs, and reserve timing. Paving distress can also reveal water-management issues that are not visible from roof records alone.

Can a property condition assessment answer every industrial exterior question?

No. A PCA can be a useful starting point, but industrial decisions may still need current photos, roof section mapping, dock and truck-court review, drainage evidence, envelope detail photos, bids, or qualified specialist review.

Sources and limits

Research basis reviewed against ASTM PCA framing, Fannie Mae PCA guidance, WBDG roofing, moisture, and building-envelope guidance, FHWA pavement preservation context, OSHA fall-protection guidance, EPA moisture-control guidance, FEMA low-slope roof mitigation guidance, NOAA/NCEI, NWS, IBHS, and BLS public sources. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence, observed condition, and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, useful life, and repair needs.

- WBDG building envelope design guideBuilding-envelope design and enclosure context for exterior wall, roof, moisture, and transition considerations.

- FHWA pavement preservationPublic pavement-preservation context for condition, timing, maintenance, and pavement-life planning.

- OSHA fall protectionOfficial workplace fall-protection context for safety boundaries around roof and exterior observation work.

- EPA moisture-control guidanceOperating and maintenance context for moisture-controlled buildings, envelope assemblies, and drainage principles.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.