Drainage risk

Roof Drains, Scuppers, Ponding Water, and Hidden Capex on Commercial Buildings

Ponding water, clogged drains, blocked scuppers, and thin maintenance records can turn a routine roof note into a hidden capital expense. This guide shows how to document drainage risk before it becomes a surprise.

Key takeaways

- Drainage risk should be reviewed as a system: drains, scuppers, gutters, overflow paths, roof slope, equipment, maintenance, and records all interact.

- Ponding water is not automatically catastrophic, but recurrence, duration, location, interior consequence, and maintenance history can turn it into a hidden capex signal.

- A buyer, lender, owner, or broker should separate known maintenance, known repair, uncertain condition, and capital correction before pricing the roof.

- The strongest drainage file connects water behavior to photos, leak history, repair chronology, maintenance records, and reserve triggers.

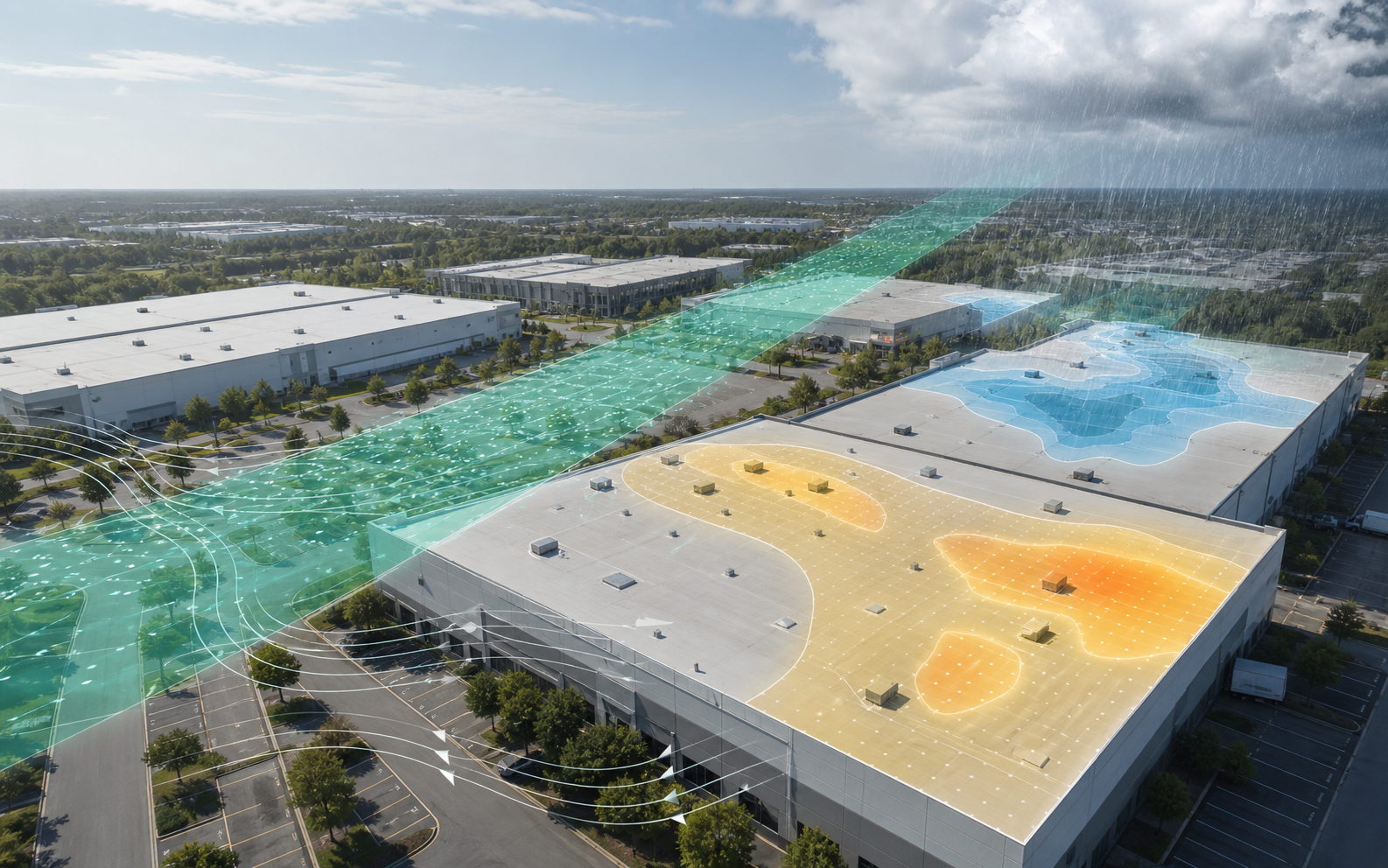

Drainage risk is a capex signal, not a cosmetic footnote

Water on a commercial roof is easy to understate when the conversation starts with age, warranty, or the last repair invoice. A building can have a newer membrane and still carry material drainage risk. Another building can have an older roof that drains cleanly, has current maintenance records, and is easier to underwrite than the newer roof. The difference is not only the roof system. It is the behavior of water, the condition of the drain paths, and the quality of the records that explain what happens after rain.

Low-slope roofs are not meant to be treated as flat trays. They are designed as assemblies that move water toward drains, scuppers, gutters, conductor heads, internal piping, or overflow paths. In practice, those paths can be interrupted by clogged strainers, blocked scuppers, added equipment, settlement, missing crickets, poor repair geometry, debris, deteriorated sealant, damaged flashing, or maintenance gaps. When water stays where the roof was not meant to hold it, the issue can become more than a roof service call. It can become a hidden capital expense.

The underwriting problem is that drainage defects often do not announce their cost at the moment of review. A roof photo may show dark staining around a drain but no open leak. A seller may report no active issues while old patch rings show that water has been a recurring concern. A property condition file may mention ponding but not map the affected area or connect it to insulation, tenant space, maintenance history, or reserve timing. A broker may say "the roof was repaired" without knowing whether the repair corrected the drainage condition or only stopped the latest leak.

Asset Optimix treats drainage as a decision signal because it connects roof condition, maintenance discipline, weather exposure, useful life, and capex confidence. The question is not whether every puddle means replacement. It does not. The question is whether the file shows that water is being managed, whether recurring wet areas are understood, and whether the reserve plan has priced the uncertainty instead of hiding it.

Ponding water needs context before it gets a conclusion

Ponding water is often discussed as though it has one meaning. In the field, it needs context. A shallow wet area shortly after rain is not the same as a deep area that remains for days. Water beside a drain after debris has accumulated is not the same as water trapped by settlement between drains. Staining around a repaired penetration is not the same as chronic water around multiple drains across a roof field. A one-time post-storm photo is not the same as a pattern documented over years.

For owners, buyers, lenders, roofers, insurers, and asset managers, the practical issue is duration, location, recurrence, and consequence. Duration asks how long water remains. Location asks where it sits relative to drains, seams, laps, penetrations, curbs, roof edges, and tenant areas. Recurrence asks whether the same location appears in inspections, leak tickets, photos, or repair invoices. Consequence asks what happens below the water: vacant storage, mission-critical operations, medical use, refrigerated space, public occupancy, records storage, retail tenants, or municipal services.

The file should avoid two shortcuts. The first shortcut is calling ponding harmless because there is no current leak. Roof assemblies can absorb risk before interior evidence appears, especially when insulation, cover board, deck conditions, or prior repairs are not documented. The second shortcut is treating every ponding mark as a replacement mandate. Some conditions can be addressed through drain cleaning, debris removal, localized repairs, crickets, tapered insulation work, scupper correction, gutter work, or a broader restoration plan. The decision depends on evidence.

A better drainage file asks:

- Where does water remain after routine rain?

- How long does it remain?

- Does the location repeat across seasons?

- Is the ponding near drains, scuppers, seams, penetrations, curbs, or edge details?

- Are there stains, biological growth, sediment rings, patch clusters, or depressed insulation?

- Do tenant leak tickets or ceiling stains align with the roof area?

- Were drains or scuppers cleaned before the observation?

- Has any repair changed the slope or trapped water?

- Has the condition been priced into reserves?

Those questions do not replace roof inspection or engineering review. They keep the business decision from becoming a guess.

Drains, scuppers, gutters, and overflow paths are a system

Commercial roof drainage is not one component. It is a system of primary drainage, secondary drainage, surface slope, openings, transitions, and maintenance access. The roof may use internal drains, scuppers through parapet walls, external gutters, conductor heads, downspouts, or combinations of these. The roof may also include emergency overflow paths intended to show when the primary drainage path is blocked or overwhelmed.

Internal drains can be efficient, but they create a documentation challenge. The roof-side strainer may look visible, but the piping below the roof deck is often out of sight. A leak near an internal drain can come from membrane tie-in failure, bowl issues, clamping ring problems, piping leaks, condensation, backup, or maintenance blockage. A buyer looking only at surface photos may miss the difference between a roof membrane issue and a plumbing or drain-line issue. A lender looking only at a remaining useful life estimate may not see that repeated interior staining aligns with a specific drain stack.

Scuppers create a different evidence profile. They are visible at parapets or roof edges, but they can be blocked, undersized for the actual roof behavior, set too high relative to the roof surface, surrounded by deteriorated flashing, or disconnected from gutters and downspouts. A scupper that appears clean in a dry photo may still be a risk if staining below the wall shows frequent overflow, if the opening has debris, or if ponding remains behind it after rain.

Gutters and downspouts are often treated as exterior maintenance items, but they can decide whether a roof behaves as designed. A clean roof surface can still suffer if gutters are clogged, pitched incorrectly, damaged, disconnected, or dumping water near the foundation. Overflow staining, soil erosion, facade stains, ice patterns, and repeated repairs at edge details can point to a roof-water management issue rather than an isolated membrane concern.

The physical underwriting file should identify the drainage path by roof section. "Roof drains present" is too thin. A stronger file says which roof areas drain to internal drains, which drain to scuppers, which rely on gutters, where overflow paths appear, what records support maintenance, and what evidence suggests the system is or is not performing.

The hidden capex problem starts when water changes the assembly

The visible cost of drainage risk may be a service call. The hidden cost can be wet insulation, damaged cover board, deteriorated deck, corroded metal, repeated patching, interior finishes, tenant interruption, mold concern, electrical or equipment exposure, or earlier roof replacement. The capex problem is not just the puddle. It is the uncertainty created when no one knows how long the assembly has been wet, what layers are affected, or whether prior repairs addressed cause or symptom.

Wet insulation is a common concern because it can reduce thermal performance, stress the membrane, complicate repairs, and change replacement scope. A roof that might otherwise be a coating or restoration candidate can become a tear-off candidate if moisture is widespread or trapped. A local drain repair can become a larger cut-out if the surrounding insulation is saturated. A buyer reserve can move materially if a condition that looked like surface staining turns into deck repair or insulation replacement.

The deck matters because the roof assembly is not only a waterproofing surface. Steel deck corrosion, wood deck deterioration, concrete deck issues, fastener pull-out concerns, or concealed substrate damage can turn a roof project into a larger structural or code-sensitive scope. A remote photo cannot resolve that. A seller statement cannot resolve that. The file has to show what is known, what is not known, and what inspection or testing would reduce uncertainty.

Repeated patching around ponding locations is especially important. It may mean the roof team kept responding to leaks without correcting drainage. It may also mean that a difficult detail was improved over time and now performs adequately. The difference matters. Patch history should be mapped by date and location. If the same drain, scupper, curb, or seam appears repeatedly, the reserve should not treat the next repair as a surprise.

For capex planning, the core question is: does the drainage condition change the likely intervention path? If the answer is yes, the reserve should include more than a generic replacement year.

Maintenance records are part of the roof asset

Drainage problems are often maintenance problems before they become capital problems. Leaves, wind-blown debris, granules, construction residue, fasteners, tenant trash, rooftop equipment filters, bird debris, vegetation, and loose materials can block strainers, scuppers, gutters, and downspouts. After major storms, reroofing work, tenant improvements, or HVAC service, the roof can carry debris that changes drainage behavior.

Maintenance records should not be treated as paperwork. They are evidence of control. A roof with annual or semiannual maintenance records, drain photos, debris removal notes, and follow-up work can be underwritten differently from a roof where nobody can prove the drains have been checked. WBDG roofing guidance and moisture-management principles both reinforce the practical point that roof performance depends on design, construction, operation, and maintenance. The roof does not stop changing after installation.

A useful maintenance file includes:

- Date of roof visit.

- Weather or season context.

- Roof areas accessed.

- Drains, scuppers, gutters, and downspouts observed.

- Debris removed.

- Strainers reset or replaced.

- Ponding areas photographed.

- Repairs performed.

- Follow-up recommendations.

- Access limitations.

- Name of contractor, facility team, or maintenance vendor.

The file should also record negative evidence when it is useful. "No debris at drains during April 2026 maintenance visit" is a meaningful statement if photos support it. It helps distinguish design or settlement issues from temporary blockage. "Drain blocked with leaves before clearing" is also useful because it explains why water was present and creates a follow-up duty.

Commercial roofers can create value by making maintenance evidence location-specific. Instead of "cleaned roof drains," a stronger note says "cleared debris from drains D-2 and D-3 on main warehouse roof; ponding stain remains east of D-3; recommend recheck after next rain." That single sentence is more useful to an owner, broker, lender, and future roofer than a generic service invoice.

Roof drains can fail in several ways

When an interior leak appears near a roof drain, the first assumption is often "roof leak." That may be correct, but the file should keep the possibilities open until the evidence is reviewed. A drain-related problem can involve the membrane tie-in, drain bowl, clamping ring, strainer, sump, piping, insulation slope, structural deflection, debris, freeze conditions, or interior plumbing. Treating every drain issue as a field-membrane problem can lead to repeated repairs that do not correct the cause.

Surface evidence can help narrow the question. A ponding ring around a drain may indicate poor slope to the drain, a blocked strainer, an elevated drain bowl, settlement, or a repair that changed water flow. Staining on the underside of a deck near a drain may indicate a roof-side issue, a pipe issue, condensation, or overflow history. Repeated interior ceiling repairs below the same drain stack should trigger a different conversation than a single wet tile after an unusual storm.

Drain bowls and clamping details deserve close attention because they are transition points between the roof membrane and the drainage system. The detail can be vulnerable when repairs are layered, clamping rings are missing or loose, strainers are broken, sealant is used as a substitute for proper detailing, or the drain is not integrated cleanly with the membrane. A surface photo may show the drain exists, but it may not show whether the tie-in is durable.

For underwriting, the best drain file does not need to prove every technical detail. It needs to separate the unknowns:

- Is water reaching the drain?

- Is the strainer clear and intact?

- Does water remain around the drain after clearing?

- Are there repeated repairs or patches near the drain?

- Are interior stains aligned with the drain or the piping path?

- Is the drain line known to be clear?

- Has a qualified party reviewed the tie-in detail?

That separation prevents a small drain detail from becoming a vague building-level roof concern. It also prevents a serious hidden condition from being dismissed because the roof is "not that old."

Scuppers and parapets can hide the real drainage condition

Scuppers look simple, which is why they are sometimes underdocumented. They are openings that allow water to exit a roof, often through a parapet wall. Their risk depends on elevation, size, flashing, wall condition, debris, downstream path, and whether overflow behavior is understood. A scupper can be present and still be poorly performing.

The first question is whether the roof surface actually directs water to the scupper. If the scupper is higher than adjacent ponding areas, water can sit elsewhere even though an outlet exists. If the roof has settled away from the scupper, the outlet may not serve the low point. If added equipment, curbs, walk pads, or repair materials interrupt the path, water may not reach the opening efficiently.

The second question is whether the scupper detail is watertight and maintainable. Deteriorated flashing, open corners, failed sealant, displaced metal, wall cracks, and staining below the opening can all matter. A parapet wall can look stable in a listing photo but carry moisture signs on the exterior face. The downstream path can matter as much as the scupper. Water that exits at a wall and runs down the facade can create other property issues.

Overflow scuppers deserve special treatment. They may not be used during routine rain, but evidence that they have carried water can signal that primary drainage was blocked or overwhelmed. Staining at overflow paths, tenant complaints after heavy rainfall, or water marks at the parapet can change the priority for drain maintenance and roof review. The point is not to make a code conclusion from a photo. It is to recognize that overflow evidence is part of the drainage story.

For brokers and owners, scupper documentation is especially useful because it is easy to photograph during pre-listing diligence. Include close-up photos, wider context photos, exterior wall evidence, downstream path, debris condition, and any ponding behind the opening. If the scupper is part of an overflow system, label it as such only when the file supports that label.

Tapered insulation, crickets, and sumps change water behavior

Drainage is shaped by geometry. Tapered insulation, crickets, saddles, sumps, and local repairs can decide whether water moves or remains. A roof plan that shows drains is not enough if the surface no longer directs water to them. Over time, added layers, recover work, insulation compression, structural movement, poorly feathered repairs, and equipment changes can create unintended low points.

Tapered insulation can be a major value driver when it is designed and installed correctly. It can improve drainage and reduce recurring wet areas. It can also become a due diligence question if the records are missing. Did a past reroof include tapered insulation? Were crickets installed behind curbs, along parapets, or between drains? Did the scope only replace membrane while preserving a poor drainage pattern? Was ponding identified before the work? Were drain elevations adjusted?

Crickets around rooftop equipment and other obstructions are a practical concern. Water that backs up behind a curb, skylight, hatch, or equipment platform can stress flashing and create local deterioration. A roof can have acceptable field drainage but poor drainage at specific obstructions. Those local areas can drive repeated leaks and repeated repairs.

Sumps around drains are another detail that should be visible in the file. A drain set too high relative to the roof surface can leave a persistent ring of water. A proper sump can help water reach the drain. But a sump detail that is patched repeatedly, clogged, or poorly integrated with membrane can become a failure point. The file should show the drain area from enough angles to understand whether the low point and outlet align.

The reserve implication is straightforward. If a roof replacement or restoration will have to correct slope or drainage geometry, the cost may be materially different from a simple surface intervention. Hidden capex often appears when the bid scope moves from membrane-only thinking to drainage correction.

Rooftop equipment and tenant work can create drainage problems

Commercial roofs are working platforms. HVAC units, exhaust fans, satellite equipment, solar attachments, refrigeration lines, gas piping, electrical conduits, communication equipment, hatches, ladders, walk pads, and tenant improvements can all affect water flow and maintenance access. A drainage file that ignores equipment is incomplete.

Equipment can create ponding in several ways. Curbs and platforms can block water paths. Condensate discharge can create persistent wet areas that look like roof drainage failure. Service traffic can compress insulation, damage membrane, or displace walk pads. Abandoned penetrations can become patch clusters. New lines can be routed across water paths. Contractors may leave debris after service. A roof that drained well at installation can perform differently after years of equipment changes.

Tenant work is especially important in retail, medical, restaurant, industrial, and multi-tenant buildings. A tenant improvement may add exhaust penetrations, refrigeration equipment, makeup air units, or other rooftop changes. If those changes are not tied back to the roof file, the owner may lose visibility into drainage and warranty responsibilities. A future buyer may see a roof with many penetrations and no clear chronology.

For physical underwriting, rooftop equipment should be connected to drainage evidence:

- Which equipment areas interrupt water paths?

- Are crickets or saddles present where needed?

- Are condensate lines routed to appropriate locations?

- Are service paths controlled with walk pads?

- Are old curbs abandoned or properly removed?

- Are drain strainers clear after equipment service?

- Do leak tickets align with equipment areas?

- Do repair invoices repeatedly mention curbs, pitch pockets, or penetrations?

This is a practical place where roofers can help owners. A roofer does not have to police every vendor. The roofer can create a repeatable post-service roof check that documents drains, debris, equipment paths, and obvious new vulnerabilities.

Interior evidence can point to drainage even when the roof photo is unclear

Some drainage problems are easier to see from inside the building than from a dry roof photo. Ceiling stains, wet insulation, tenant work orders, odor complaints, corrosion, rust trails, peeling finishes, damaged ceiling tiles, or recurring buckets can reveal patterns that surface photos miss. The key is mapping the interior evidence to the roof plan without jumping to conclusions.

Interior evidence should be recorded by location, date, weather context, tenant space, roof area above, and follow-up action. A stain near a drain stack after heavy rain may suggest a drain or pipe issue. A stain below a curb may suggest flashing or equipment issues. A stain that appears after snow melt may indicate a different exposure than a stain that appears only during wind-driven rain. The words "roof leak" in a tenant ticket are a starting label, not a technical conclusion.

Owners should preserve the sequence. When did the leak appear? Was it after routine rain, heavy rain, wind-driven rain, snow melt, HVAC service, plumbing work, or roof access? Was the drain blocked? Was the roof inspected while water was present? Was the ceiling repaired before the roof cause was documented? Was the same area repaired before?

For lenders and buyers, interior evidence matters because it affects consequence. A small roof issue over vacant storage may be manageable. The same issue over a medical office, production line, data room, food service tenant, school, or public records area can change the urgency. The reserve should reflect more than roof square footage. It should reflect what happens if water enters the building.

Interior mapping also protects sellers and brokers from vague statements. Instead of saying "no roof issues," a better file can say "two tenant leak tickets in Suite 104 during 2025; repairs completed near drain D-4; no subsequent tickets through April 2026; current roof photos pending." That is more credible than silence and more useful than overconfidence.

Weather exposure changes the priority of drainage review

Rainfall history matters, but it should not be used loosely. Heavy rainfall, tropical systems, severe thunderstorms, freeze-thaw cycles, hail, and wind can expose weaknesses in drainage systems. NOAA and National Weather Service records can help identify exposure context, and local rain history can explain why a roof received stress. Those records do not prove that a specific roof drain, scupper, or membrane detail failed. Property-specific evidence still matters.

The practical use of weather exposure is priority. If a property experienced significant rainfall and the roof has stale photos, unknown drain maintenance, and tenant leak tickets, the roof deserves a current drainage review. If a severe wind event occurred and edge scuppers, parapets, and gutters have not been photographed since then, the file should request updated evidence. If a roof has an unknown age and a history of heavy rain exposure, the reserve should include uncertainty until the condition is known.

Weather exposure should be connected to response evidence. A strong file says what happened after the event: drains checked, debris removed, scuppers photographed, leak tickets reviewed, repairs made, roof consultant engaged, or no roof access available. The absence of a claim, absence of a leak ticket, or absence of a repair invoice does not automatically prove the roof was unaffected. It may simply mean the roof was not checked or the records are incomplete.

Drainage review after major rainfall should focus on the physical path of water:

- Are primary drains clear?

- Are overflow paths visible and unobstructed?

- Are scuppers free of debris?

- Are gutters and downspouts moving water away?

- Are there new sediment rings, stains, or ponding marks?

- Did water enter tenant spaces?

- Did equipment areas create runoff or condensate patterns?

- Were temporary repairs made?

Weather context improves the decision when it is tied to roof vulnerability and records. It weakens the decision when it is used as a substitute for roof evidence.

Property condition assessments need roof-specific drainage support

Property condition assessments can be valuable in commercial transactions and lending, but roof drainage often needs more detail than a broad building review can provide. ASTM E2018 provides a general framework for property condition assessments. Fannie Mae multifamily guidance includes property condition and reserve concepts. Those frameworks help organize diligence, but they do not guarantee that every roof drain, scupper, ponding area, or hidden moisture concern has been resolved.

The issue is scope. A PCA may involve visual observation, representative sampling, limited access, interviews, document review, and estimated useful life judgments. If roof access is limited, weather is dry, drains are not inspected closely, or records are thin, a drainage condition may be understated. A remaining useful life number may not capture the cost of correcting drainage geometry, replacing wet insulation, or resolving repeated drain leaks.

Buyers and lenders should treat PCA roof comments as a starting point:

- Was the roof accessed directly?

- Were all roof areas visible?

- Were drains and scuppers photographed?

- Was ponding observed or only inferred from staining?

- Were leak logs reviewed?

- Were repair invoices reviewed?

- Were roof sections and ages separated?

- Was moisture testing performed or excluded?

- Were maintenance records available?

- Were reserve recommendations tied to drainage concerns?

The goal is not to criticize the PCA. The goal is to know what it actually supports. If the PCA says the roof appeared serviceable but also says access was limited and no maintenance records were reviewed, the drainage risk may remain open. If the PCA maps ponding and recommends further evaluation, that recommendation should be carried into the reserve and negotiation file.

Buyers should price uncertainty separately from known repair cost

In acquisitions, drainage risk often appears as uncertainty rather than a clean known cost. A seller may provide a roof repair invoice for a drain leak. The buyer may see ponding stains in photos. The lender may receive a PCA with a roof reserve. The insurance broker may ask for roof age and condition. None of those items alone answers the financial question.

Buyers should separate four buckets:

| Bucket | Example | Decision use |

|---|---|---|

| Known maintenance | Drains need cleaning, gutters need debris removal | Operating action and vendor scheduling |

| Known repair | Failed scupper flashing, broken strainer, local membrane tie-in | Immediate repair scope and seller credit discussion |

| Uncertain condition | Ponding history with no moisture scan or current photos | Inspection, testing, reserve contingency |

| Capital correction | Tapered insulation, drain relocation, wet insulation removal, replacement | Capex plan, loan reserve, price adjustment |

The mistake is to treat uncertain condition as zero cost because no bid exists. The opposite mistake is to price the entire roof as failed when the issue may be localized. A useful buyer file keeps the buckets visible and requests the evidence that would move an item from uncertain to known.

For 1031 exchange buyers, this matters because timing pressure can turn open roof questions into closing risk. A late discovery of wet insulation or unresolved ponding can affect lender conditions, insurance questions, seller negotiations, and reserve comfort. The existing [commercial roof records before a 1031 exchange acquisition guide](/insights/commercial-roof-records-1031-exchange-acquisition/) explains why roof records should be gathered early when replacement-property timing is tight.

Drainage should be part of that early file. It is not a specialty question to save for the end.

Lenders need evidence quality, not just a replacement year

Lenders often receive roof information as age, remaining useful life, immediate repair cost, and reserve recommendation. Those fields are useful, but they can hide drainage uncertainty. A roof may have ten years of estimated remaining life and still have an unaddressed ponding area over a critical tenant. Another roof may have a near-term replacement recommendation but excellent drainage records and a clear reserve plan. The risk posture is different.

A lender-focused drainage review should ask whether the collateral file supports the roof conclusion. If the building has low-slope roofs, internal drains, parapets, tenant operations, and limited records, the lender may need more than an age estimate. The file should show whether drains and scuppers were observed, whether roof access occurred, whether leak history was reviewed, whether ponding areas were mapped, and whether immediate repairs or reserves include drainage correction.

This is especially important for properties with high tenant consequence. Water intrusion can affect rent, operations, borrower liquidity, insurance discussions, and property value. The lender does not need to become a roof consultant. The lender needs a defensible basis for whether roof risk is routine, conditionally acceptable, or a reserve/repair condition.

A practical lender note might say:

| Evidence state | Lender posture |

|---|---|

| Current roof photos, clear drain maintenance, no recurring leaks, reserve supported | Routine monitoring |

| Ponding photos, no leak history, maintenance records missing | Request maintenance evidence or roof review |

| Repeated drain leaks, tenant disruption, no moisture testing | Consider repair condition or reserve adjustment |

| Wet insulation confirmed, drainage correction needed | Require scope, bids, reserve, or closing condition |

The right action depends on the loan, property, borrower, and professional review. The point is that drainage evidence should not disappear behind a single useful-life number.

Brokers can reduce deal friction with a drainage file

Brokers do not need to certify roof condition. They do need to avoid vague roof statements that invite buyer distrust. A pre-listing drainage file can help a broker market the building without overclaiming and can help serious buyers move faster through diligence.

The drainage file should be practical:

- Current roof photos after the roof is cleaned.

- Close-ups of drains, scuppers, gutters, and overflow paths.

- Any known ponding areas and dates observed.

- Leak log or seller statement on leak history.

- Recent roof maintenance invoices.

- Roof repair invoices by location.

- Warranty and maintenance obligations if available.

- PCA roof excerpts if a recent PCA exists.

- Known bids or planned work.

- Access limits or areas not reviewed.

The broker should be careful with language. "New roof" is not a substitute for scope. "No known leaks" is not a drainage assessment. "Seller reports roof repairs were completed in 2024" is more defensible when the invoice and location are included. If ponding exists, saying nothing may create more trouble than disclosing the evidence and the seller's response.

The existing [broker listing diligence guide for buildings with flat roofs](/insights/commercial-roof-broker-listing-diligence/) covers the broader pre-listing roof file. Drainage deserves its own emphasis because water behavior is one of the easiest things for buyers to question from photos, satellite history, and tenant interviews.

Owners should manage drainage as an operating control

Owners and facility managers have the most control over drainage risk because they control access, maintenance, vendor coordination, and recordkeeping. The roof should have a seasonal drainage routine, especially before and after periods of heavy rain, leaf fall, snow, or major rooftop work.

A basic owner workflow includes:

- Keep roof access controlled and documented.

- Clean drains, scuppers, gutters, and downspouts on a routine schedule.

- Recheck drainage after storms and after rooftop service work.

- Photograph recurring ponding areas from the same angles.

- Map leaks to roof areas and drainage paths.

- Keep invoices and maintenance notes by roof section.

- Require rooftop vendors to report debris, damage, or blocked paths.

- Review whether condensate lines discharge appropriately.

- Update the reserve when drainage behavior changes.

The owner should also decide who owns the follow-up. A property manager may create the work order. A facility team may clear debris. A roofer may inspect the membrane and details. A plumbing contractor may review drain lines. A consultant or engineer may evaluate structural or persistent drainage questions. Ambiguity is the enemy. If no one owns the path from observation to decision, the same wet area can persist for years.

Owners should not wait for a transaction to organize this evidence. A clean drainage file helps with lender renewals, insurance questions, tenant complaints, capital planning, and emergency response. It also gives roofers better context, which can reduce wasted visits and repeated repairs.

Roofers can turn drainage observations into advisory value

Commercial roofers often see drainage evidence before anyone else understands its financial meaning. A technician may clear a clogged drain, note ponding at a scupper, see sediment rings around a repair, or notice that equipment service has blocked a water path. If those observations stay in memory or vague invoice language, the owner loses value.

The advisory opportunity is to make drainage observations decision-ready:

- Use roof area names or drain IDs where possible.

- Photograph from context view and close-up view.

- Identify whether debris was removed before or after the photo.

- Note whether water remains after clearing.

- Connect repeated service calls to the same location.

- Separate immediate repair from recommended evaluation.

- Avoid overstating cause when evidence is incomplete.

- Recommend next action in plain language.

For example, "Cleared drain" is weak. "Cleared drain D-2 on north warehouse roof; standing water remained in a low area east of drain after debris removal; recommend post-rain review and owner discussion about slope correction options" is much more useful. It helps the owner understand why maintenance may not be enough. It also helps a future buyer, lender, or asset manager see that the roofer identified cause uncertainty rather than simply selling a replacement.

Roofers should also be careful around weather and insurance language. A storm may have exposed a drainage weakness, but the roofer should not turn exposure context into unsupported conclusions. The existing [roof weather risk and physical underwriting guide](/insights/roof-weather-risk-physical-underwriting/) explains how to use weather history without treating it as property-specific proof.

Insurers and risk engineers should separate drainage maintenance from roof condition

Insurance teams and risk engineers may see drainage as part of broader property risk: water intrusion, wind-driven rain, roof vulnerability, tenant interruption, and maintenance discipline. The file should distinguish a one-time maintenance issue from a chronic roof-condition concern.

A blocked drain after leaf fall is not the same as chronic ponding caused by roof settlement. A cracked scupper flashing is not the same as an undersized or poorly located drainage path. Repeated leaks near internal drains are not the same as a single plumbing incident. The difference matters because it changes recommendations, follow-up, and confidence.

Risk review can organize drainage into:

- Maintenance control: debris, strainers, gutters, access, vendor practices.

- Roof assembly condition: membrane tie-ins, seams, wet insulation, patches.

- Drainage design or geometry: slope, tapered insulation, drain elevation, scupper location.

- Consequence: occupancy, tenant operations, interior finishes, business interruption.

- Evidence quality: current photos, records, access, inspection scope, unresolved unknowns.

This structure helps avoid overreaction and underreaction. It also helps risk teams communicate with owners and brokers in a way that produces action. "Clean drains quarterly and provide photos" is a different recommendation from "evaluate chronic ponding and wet insulation around main roof drains." Both may be valid in different cases.

Municipal and public portfolios need triage discipline

Municipalities, school districts, public agencies, and nonprofit portfolios often manage multiple low-slope roofs with constrained budgets. Drainage risk can quietly consume maintenance funds because small recurring leaks, interior repairs, and emergency calls are spread across many buildings. The portfolio team needs triage discipline, not just a list of roof ages.

A portfolio drainage screen should combine roof age, drainage type, leak frequency, tenant or public-service consequence, maintenance records, recent weather exposure, and known capital plans. A library roof with public records below a chronic ponding area may deserve priority over a storage building with an older roof but clean drainage history. A school roof with repeated drain backups after heavy rain may need a different intervention than a city garage with isolated gutter maintenance.

Public owners should also preserve institutional memory. Staff changes can erase knowledge of which drains clog, which scuppers overflow, which classrooms receive ceiling stains, and which repairs were temporary. A simple roof-area map with drain IDs, photos, and maintenance notes can keep the next budget cycle from starting over.

Because public procurement and engineering requirements vary, the drainage file should not pretend to replace professional review. It should help the agency decide where qualified review, maintenance dollars, and capital planning attention should go first.

A practical drainage photo set

Drainage decisions improve quickly when the photo set is consistent. Random roof photos create confusion. A practical set gives each stakeholder the same visual evidence and makes future comparisons possible.

For each roof area, capture:

| Photo | Purpose |

|---|---|

| Wide roof area view | Shows drainage layout, equipment, parapets, and surface condition |

| Each primary drain | Shows strainer, sump, debris, ponding, tie-in, and nearby patches |

| Each scupper | Shows opening, flashing, debris, elevation, and parapet context |

| Overflow paths | Shows whether secondary paths are visible and unobstructed |

| Gutters and downspouts | Shows downstream path, clogging, damage, or facade staining |

| Ponding locations | Shows depth clues, sediment rings, biological growth, and location |

| Rooftop equipment | Shows curbs, condensate, service paths, and water interruption |

| Interior stains | Connects roof evidence to tenant or operational consequence |

When possible, take repeat photos from the same position. The best photo set compares dry conditions, post-rain conditions, and post-maintenance conditions. If water remains after drains are cleared, the file should say so. If a photo was taken before debris removal, the file should say that too.

Do not edit photos to make the condition look better or worse. Do not crop away context that a reviewer needs. Do not rely only on close-ups. The wide view explains where the close-up belongs.

Drainage reserve triggers should be explicit

A roof reserve becomes more useful when it has triggers. Drainage triggers tell the owner, buyer, lender, or asset manager when the plan should change. Without triggers, the reserve is just a number waiting to be surprised.

Practical triggers include:

- Water remains in the same area after routine rain and drain cleaning.

- Ponding appears near seams, laps, penetrations, or curbs.

- The same drain or scupper appears in multiple repair invoices.

- Tenant leak tickets align with a drainage path.

- Wet insulation is confirmed or suspected by qualified review.

- Drain strainers are missing, broken, or repeatedly clogged.

- Overflow scuppers show staining or active use during routine events.

- A roof replacement bid includes tapered insulation or drainage correction not previously reserved.

- A PCA notes ponding but does not include roof-specific follow-up.

- Major weather exposure occurs after the last roof condition file.

Each trigger should have an action. The action may be maintenance, roof review, moisture testing, bid refresh, reserve adjustment, seller request, lender discussion, or immediate repair. A trigger without an action is only a note.

This ties directly into the broader [commercial roof capex and reserve planning guide](/insights/commercial-roof-capex-reserve-planning/). Drainage is one of the clearest ways roof uncertainty turns into capital timing.

A simple decision matrix for ponding and drainage risk

The decision should reflect evidence, not fear. A simple matrix can help teams keep the next action proportional.

| Evidence pattern | Likely posture | Practical next action |

|---|---|---|

| Clear drains, no recurring ponding, current maintenance photos | Routine control | Continue scheduled maintenance and photo records |

| Debris-blocked drains, water resolved after cleaning | Maintenance issue | Increase cleaning cadence and recheck after rain |

| Ponding remains after cleaning, no leaks, no moisture evidence | Condition uncertainty | Schedule roof review and update reserve confidence |

| Ponding near seams, curbs, or repeated patches | Elevated roof concern | Map repairs, inspect details, consider moisture testing |

| Repeated leaks near drain or scupper | Active risk | Review drain/scupper detail, interior path, and repair scope |

| Wet insulation or deck concern confirmed | Capital issue | Price scope, reserve, and qualified intervention |

| Drainage correction required for replacement or restoration | Capex planning issue | Obtain scope options and align budget timing |

The matrix is not a substitute for a qualified roof decision. It is a communication tool. It helps an owner explain why a cleaning action is enough in one case and why a deeper review is required in another.

What not to conclude from drainage evidence

Drainage evidence is powerful, but it has limits. A photo of ponding does not prove the membrane has failed. A clogged drain does not prove the roof was poorly installed. A scupper stain does not prove the roof is beyond repair. A weather record does not prove that water entered the building. An interior stain does not prove the roof was the only source. A roof age does not prove remaining useful life.

The file should avoid warranty conclusions unless the warranty documents and qualified parties support them. It should avoid code conclusions unless a qualified professional reviews the applicable requirements. It should avoid insurance coverage conclusions. It should avoid engineering conclusions from photos alone. It should avoid calling a roof replacement necessary when the evidence supports only maintenance or further evaluation.

The better language is disciplined:

- "Observed ponding stains near drain D-3; duration unknown."

- "Owner reports drain was cleared after photo; post-cleaning condition not documented."

- "Repeated leak tickets align with east scupper area; roof-specific review recommended."

- "Wet insulation has not been confirmed; moisture evaluation would reduce uncertainty."

- "Reserve should include drainage-correction contingency until scope is known."

That style does not weaken the file. It makes the file more reliable.

The strongest drainage file connects water, records, and money

Drainage is one of the best tests of commercial roof discipline because it touches every stakeholder. Roofers see the field evidence. Owners control maintenance. Brokers manage disclosure and buyer questions. Buyers price uncertainty. Lenders review collateral risk. Insurers and risk engineers look for water-intrusion vulnerability. Asset managers translate condition into reserves. Public owners triage limited capital across many buildings.

The strongest file does three things. First, it shows how water leaves each roof area: drains, scuppers, gutters, overflow paths, and the surface geometry that connects them. Second, it shows whether that system is maintained: cleaning records, photos, vendor notes, repair history, and post-weather response. Third, it shows how uncertainty changes money: immediate repairs, inspection needs, reserve timing, capital correction, and tenant consequence.

Ponding water, clogged drains, and scupper stains are not automatically catastrophic. They are evidence. The business risk appears when evidence is ignored, flattened into a generic roof age, or left out of the reserve. A commercial roof does not need perfect records to be underwritten, bought, financed, insured, or maintained. It needs honest records that show what is known, what remains unknown, and what action follows.

When a drainage file reaches that standard, hidden capex becomes less hidden. The team can decide whether the next step is cleaning, repair, inspection, moisture evaluation, reserve adjustment, or broader roof planning. That is the difference between reacting to water after it reaches the tenant and managing the roof as an asset before the next decision depends on it.

Frequently asked questions

Does ponding water always mean a commercial roof needs replacement?

No. Ponding water needs context: duration, recurrence, location, maintenance condition, interior consequence, and whether moisture or deck concerns are present. Some issues may be maintenance or localized repair items, while chronic ponding can require deeper review or capital planning.

Why do lenders and buyers care about roof drains and scuppers?

Drains and scuppers show whether water is being managed. Blockage, repeated repairs, ponding, overflow staining, or missing maintenance records can reduce confidence in roof useful life, reserve timing, tenant risk, and acquisition pricing.

What records help prove commercial roof drainage is being managed?

Useful records include current roof photos, drain and scupper close-ups, cleaning logs, leak tickets, repair invoices by location, post-weather checks, maintenance recommendations, and notes on access limits or unresolved ponding.

Sources and limits

Research basis reviewed against WBDG roofing and moisture guidance, FEMA low-slope roof mitigation guidance, EPA moisture-control guidance, ASTM PCA framing, Fannie Mae PCA guidance, NOAA/NCEI, NWS, IBHS, and BLS public sources. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence, observed condition, and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, useful life, and repair needs.

- EPA moisture-control guidanceOperating and maintenance context for moisture-controlled buildings, including low-slope roof drainage principles.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.